Saving for retirement can feel overwhelming when you first start working. Many Americans hear terms like “401(k),” “employer match,” or “vesting schedule” but are unsure what they mean.

The good news is that understanding a 401(k) is easier than it sounds, and getting started early can make a significant difference over time.

Looking for the full breakdown? See our Complete 401(k) Guide (2026) for contribution limits, rollovers, and detailed tax rules.

Quick Answer

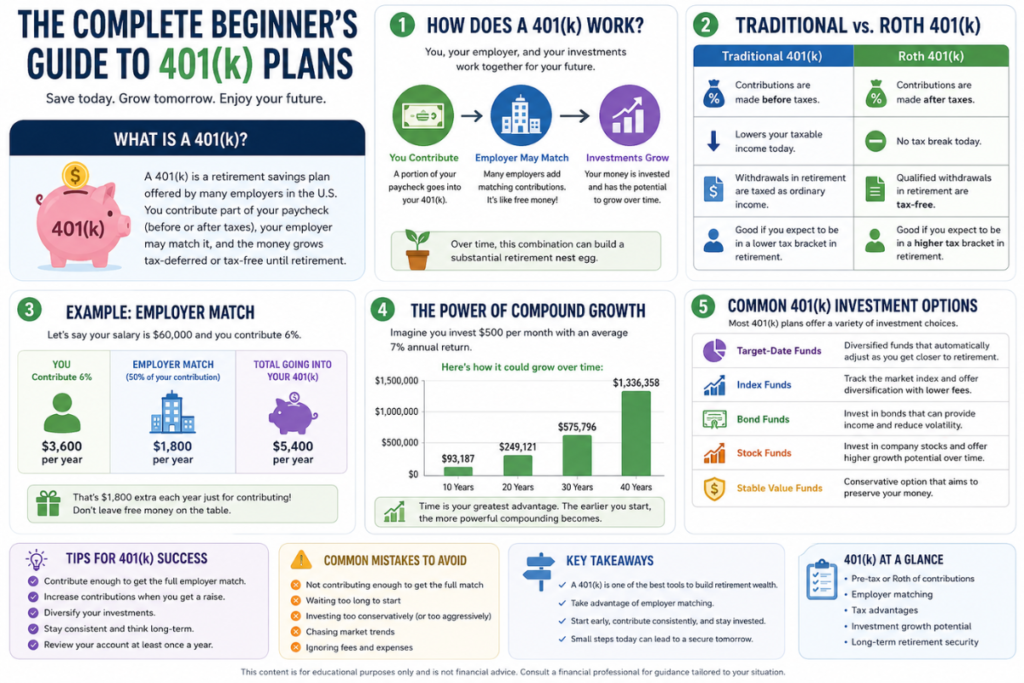

A 401(k) is a retirement savings account offered by many employers in the United States. Employees can contribute part of their paycheck into the account, often before taxes are deducted, and many employers also contribute money through matching programs. The investments inside the account can grow over many years, helping workers build savings for retirement.

What Is a 401(k)?

A 401(k) is an employer-sponsored retirement plan named after a section of the U.S. tax code. Instead of relying only on Social Security or personal savings, workers can regularly invest money from their paychecks into long-term investments.

The money is typically invested in options such as:

- Stock mutual funds

- Bond funds

- Target-date retirement funds

- Index funds

- Stable value funds

The goal is to let investments grow over decades while offering valuable tax advantages.

Why Is a 401(k) Important?

Many financial experts believe a 401(k) is one of the easiest ways to build wealth for retirement.

Benefits include:

- Automatic payroll deductions

- Potential employer matching contributions

- Tax advantages

- Long-term compound growth

- Professional investment options

- Convenient automatic investing

Even relatively small monthly contributions can grow substantially over several decades.

How Does a 401(k) Work?

A percentage of your paycheck is automatically deposited into your retirement account before you receive your salary.

For example:

| Annual Salary | Employee Contribution | Employer Match | Annual Total Invested |

|---|---|---|---|

| $60,000 | 6% ($3,600) | 3% ($1,800) | $5,400 |

Your money is then invested according to the options you select.

Over time:

- Contributions accumulate.

- Investment returns compound.

- Dividends may be reinvested.

- Employer contributions increase your balance.

Traditional 401(k) vs. Roth 401(k)

| Feature | Traditional 401(k) | Roth 401(k) |

| Contributions | Pre-tax | After-tax |

| Taxes Today | Lower taxable income | No immediate tax break |

| Taxes in Retirement | Usually taxable | Qualified withdrawals generally tax-free |

| Best For | Workers seeking tax deductions now | Workers expecting higher future tax rates |

Some employers offer both options, allowing employees to choose based on their financial goals.

What Is Employer Matching?

Employer matching is often described as “free money.”

For example:

- You contribute 6% of your salary.

- Your employer matches 50% of that amount.

- Your retirement savings increase without requiring additional work.

Some companies match:

- Dollar-for-dollar up to a limit

- 50 cents per dollar contributed

- Fixed percentages based on company policy

Failing to contribute enough to receive the full employer match may mean leaving part of your compensation unclaimed.

Understanding Vesting

Employer contributions may become yours immediately or over time.

A vesting schedule determines how much of the employer’s contributions you own if you leave the company.

Example:

| Years Worked | Employer Contribution You Keep |

| 1 Year | 20% |

| 2 Years | 40% |

| 3 Years | 60% |

| 4 Years | 80% |

| 5 Years | 100% |

Your own contributions are always yours.

What Can You Invest In?

Most plans offer diversified investment choices.

Common options include:

Target-Date Funds

These automatically adjust risk as you approach retirement age.

Pros

- Simple

- Professionally managed

- Automatic diversification

Cons

- Limited customization

Index Funds

These track major market indexes and often have relatively low fees.

Advantages:

- Broad diversification

- Lower expenses

- Long-term growth potential

Bond Funds

Bond investments generally seek income and may experience less volatility than stocks, although they still carry risk.

Stock Funds

Stock-focused investments may provide higher long-term growth potential but can fluctuate significantly in value.

How Much Should You Contribute?

Financial situations differ, but many planners suggest:

- Contribute enough to receive the full employer match.

- Increase contributions whenever you receive raises.

- Stay consistent over the long term.

Automatic annual increases of 1% can make saving easier without requiring major lifestyle changes.

The Power of Compound Growth

Imagine investing:

- $500 per month

- For 30 years

- With an average annual return of 7%

You could accumulate hundreds of thousands of dollars through consistent investing and reinvested earnings.

The earlier you begin, the more time compound growth has to work.

Tax Advantages

Traditional 401(k):

- Contributions may reduce taxable income today.

- Taxes are generally paid when money is withdrawn in retirement.

Roth 401(k):

- Contributions are made with after-tax dollars.

- Qualified withdrawals in retirement are generally tax-free.

Always consider your personal tax situation when choosing between them.

What Happens If You Change Jobs?

Your retirement savings do not disappear.

Common options include:

- Leave the account with your former employer (if permitted)

- Roll it into a new employer’s plan

- Roll it into an IRA

- Cash out (often resulting in taxes and possible penalties)

Rolling over retirement assets can help preserve tax advantages and avoid unnecessary costs.

Can You Withdraw Money Early?

Generally, withdrawing funds before retirement age may trigger taxes and additional penalties unless an exception applies.

Because retirement accounts are designed for long-term saving, early withdrawals can significantly reduce future wealth.

Common Mistakes Beginners Make

1. Ignoring Employer Matching

Missing matching contributions means missing a valuable benefit.

2. Waiting Too Long

Time is one of the most powerful factors in retirement investing.

3. Investing Too Conservatively

Keeping all retirement money in cash-like investments may reduce long-term growth potential.

4. Chasing Market Trends

Frequently buying investments after sharp price increases or selling during downturns can hurt long-term performance.

5. Forgetting Fees

Investment expenses can reduce returns over many years.

How Market Ups and Downs Affect Your 401(k)

Retirement accounts are invested in financial markets, so balances can rise and fall.

Short-term declines are normal.

Historically, long-term investors who remain diversified and continue contributing have often recovered from market downturns over time, though future performance is never guaranteed.

Should Young Workers Start Immediately?

For many people, yes.

Someone who starts investing at age 25 may have decades for contributions and investment gains to compound before retirement.

Waiting until age 40 often requires much larger contributions to pursue similar retirement goals.

Should Older Workers Still Contribute?

Absolutely.

Even workers nearing retirement may benefit from:

- Employer matching

- Tax advantages

- Additional years of investment growth

- Catch-up opportunities when permitted under applicable rules

How to Choose Investments as a Beginner

If you’re new to investing:

- Consider diversified funds instead of individual stocks.

- Review your risk tolerance.

- Understand your expected retirement timeline.

- Rebalance periodically if needed.

Many beginners appreciate target-date funds because they automatically adjust asset allocation over time.

Is a 401(k) Better Than a Savings Account?

For retirement goals, many people use a 401(k) because it offers tax benefits and investment opportunities that may provide higher long-term growth than keeping cash in a standard savings account.

However, savings accounts remain important for emergency funds because retirement accounts are intended for long-term investing.

Example Retirement Journey

Sarah begins contributing at age 24.

- Salary: $55,000

- Contribution: 8%

- Employer Match: 4%

She increases contributions after promotions and stays invested through market ups and downs.

Over several decades, disciplined saving and long-term investing help build a substantial retirement portfolio.

While individual results vary, consistency often plays a larger role than trying to perfectly time markets.

Key Takeaways

- A 401(k) is a workplace retirement savings plan.

- Employer matching can significantly increase retirement savings.

- Starting early gives compound growth more time to work.

- Diversification helps manage investment risk.

- Avoid unnecessary early withdrawals when possible.

- Regular contributions and patience are often more important than predicting short-term market movements.

Table of Contents

Read More

Beginner Investing Guide: How to Start Investing in 2026

Complete Oil Price Timeline: History, Crashes, Booms & Global Events (1970–2026)

What is a 401(k) in simple words?

It is a retirement savings plan offered by many employers that lets workers invest part of their paycheck for future retirement while receiving valuable tax benefits.

Is employer matching free money?

Employer matching is generally considered part of your compensation package. If available, contributing enough to earn the full match can substantially increase retirement savings.

Can I lose money in a 401(k)?

Yes. Investments inside a 401(k) can decline in value because markets fluctuate. Diversification and a long-term perspective may help manage this risk.

What happens if I quit my job?

You usually keep your own contributions and may be able to leave the account where it is, roll it into another retirement account, or transfer it to a new employer’s plan, depending on the circumstances.

Should beginners choose a target-date fund?

Many beginners appreciate target-date funds because they automatically maintain diversified portfolios and gradually become more conservative as retirement approaches.

Can I have both a 401(k) and an IRA?

Yes. Many Americans contribute to both, although eligibility rules and tax treatment can vary.

Final Thoughts

A 401(k) remains one of the most effective tools available to U.S. workers for preparing for retirement. By contributing consistently, taking advantage of employer matching when available, selecting diversified investments, and staying focused on long-term goals, beginners can build a strong foundation for financial security.

Retirement planning does not require perfect timing or expert stock-picking. In many cases, the combination of steady saving, disciplined investing, and patience is what makes the biggest difference over the course of a career.

Disclaimer: The information in this article is provided for educational and informational purposes only and should not be considered financial, investment, tax, or legal advice. While we strive to keep our content accurate and up to date, laws, regulations, and retirement plan rules may change over time. Individual financial situations vary, and the strategies discussed may not be suitable for everyone. Before making decisions about your 401(k), retirement savings, investments, or taxes, consider consulting a qualified financial advisor, tax professional, or your employer’s plan administrator. Investing involves risk, including the potential loss of principal, and past performance does not guarantee future results.

Emily Rodriguez covers corporate earnings, deals, and company news for Wall Street Sights, with a focus on what business decisions mean for investors and consumers.